公关 PR

健康 HEALTH

咨询 CONSULTING

消费者体验 EXPERIENCE

公关 PR

健康 HEALTH

咨询 CONSULTING

消费者体验 EXPERIENCE

Seven months into the pandemic, uncertainty is still prevalent among consumers worldwide. Slower than anticipated economic recovery from COVID-19 and fears of a second wave have consumers tightening their belts and cutting deep into their spending. This has affected different industries to varying degrees, with some FMCG brands hoping to recover by the end of this year, while some in the luxury sector may not fully recover until as late as the second half of 2021.

Weathering a storm of such magnitude requires brands to focus their efforts on their high-value customers, or in the words of Joseph Juran himself, the "vital few". As acquiring a new customer is substantially more expensive than retaining an existing one, doing so can allow brands to boost their ROI as they navigate the crisis. Yet, in the wake of unprecedented socio-economic shifts, brands must look beyond the monetary value of transactions when identifying these customers.

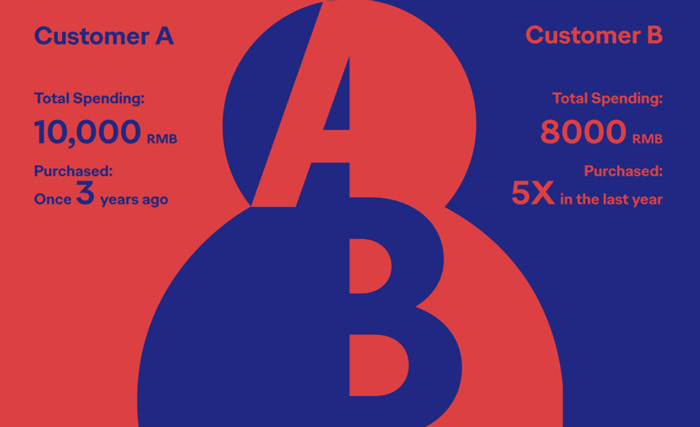

Is Customer A or Customer B more valuable to the brand? To only consider their total spending would be too one-sided. In order to effectively assess how profitable a customer is, brands usually turn to the RFM methodology, a customer segmentation tool which takes into account the three following metrics:

The most profitable customers are those who perform highly across all three aspects of the RFM model. While the traditional RFM model remains an effective tool to assess customer value, the post-COVID era offers new opportunities for brands to identify and target customers who might have otherwise been overlooked.

Here, we take a deep dive into the luxury and FMCG industries, looking at how brands can adjust their segmentation strategy in the "New Normal".

Traditionally, luxury brands focus on the monetary dimension when identifying their highest-value customers, targeting clients who have higher discretionary spending power. In a post-pandemic landscape however, recency is an equally important metric to consider in light of the significant changes that occurred in luxury consumers' buying behavior in the last few months. Specifically, we've seen two types of consumers emerge:

The Ones Who Stayed Calm and Carried On

The pandemic has brought a decade of undeterred growth in the luxury sector to an abrupt halt in just a few weeks. In a recent report, BCG modeled two scenarios to predict market recovery in the upcoming 2 years (Chart 1): an optimistic scenario with a quicker consumption rebound due to effective epidemic management and bullish consumer sentiment, and a pessimistic scenario that would see the industry bounce back at a much slower pace.

While we witnessed a significant dip in Chinese consumers' luxury spending, initial observations indicate that the personal luxury market in China is following the best-case scenario path, recovering faster than the rest of the world thanks to a few key customers who continued to purchase despite the difficult economic climate.

These true luxury enthusiasts may be reducing their spending this year, but they will likely resume their normal levels of spending in 2021. In a post-COVID context, a loyal customer who consistently buys is more valuable for a brand than a customer who may have previously bought a big-ticket item but has not purchased anything since.

Brand Opportunity: Faced with loyal customers who are temporarily forced to reduce their discretionary expenses, brands can find creative ways to trigger new purchases, either by upselling them with early access to limited edition products or by introducing them to new services that can better meet novel, COVID-19 induced consumer needs.

The "Newcomers" Who Aren't So New

With overseas travel still deeply affected by entry restrictions, 73% of Chinese consumers are expecting to repatriate at least half of their yearly abroad luxury spend back to China in the coming year. This could result in the China luxury market to grow even faster than anticipated pre-COVID (Chart 2).

Some consumers may even be purchasing luxury products domestically for the first time – forecasts indicate that luxury sales on the Mainland could grow up to 5% this year, compared to a 45% contraction globally. This is a good opportunity for luxury brands to build affinity with Chinese consumers and ensure they keep buying locally even after international travel reopens.

Brand Opportunity: While Chinese consumers previously did most of their luxury shopping overseas, the unlikely resumption of international travel for the foreseeable future means that luxury brands need to be agile in shifting their engagement approach, highlighting the premium shopping experience they can enjoy when purchasing closer to home instead. This can be done by offering China-based shoppers more personalized services and benefits such as invitations to exclusive brand events to incentivize them to keep purchasing within China.

In the FMCG sector, brand loyalty is relatively low as the products involved are easily replaceable - customers who repeatedly buy from the same brand over time will thus be considered more valuable. However, COVID-19 has dampened consumer sentiment and drastically changed shopping behaviors, forcing FMCG brands to look beyond frequency as their primary indicator to identify their highest-value customer segment.

Those Who Prepared For the Worst

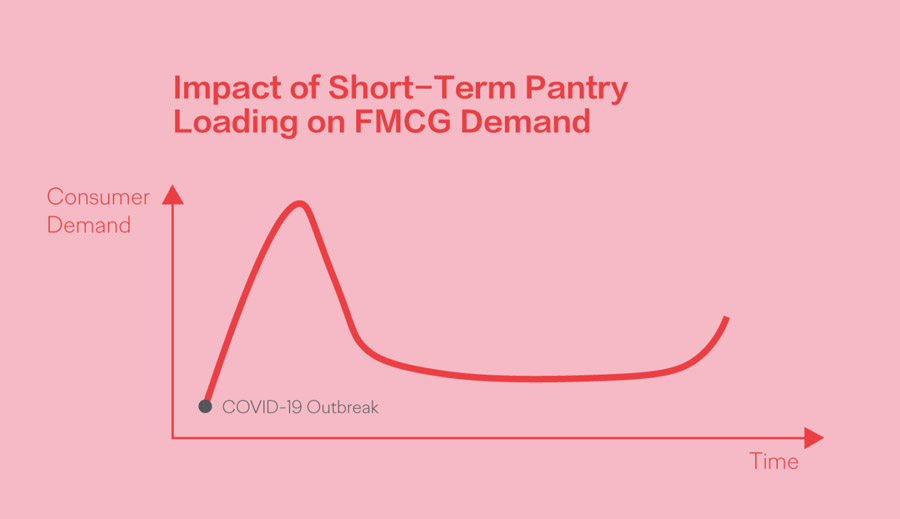

FMCG brands, especially those in the household essentials category, witnessed dramatic changes in purchasing behavior as customers stockpiled on groceries and daily necessities in the weeks that followed the outbreak. This will cause consumers' purchase frequency to drop, or even stop completely, for the rest of the year (Chart 3).

We should nonetheless keep considering them as high-value customers, as their decision to purchase in bulk shows solid loyalty to the brand. The fickle nature of FMCG consumers makes it critical for brands to sustain this relationship and stay top-of-mind for customers throughout the year; otherwise, they will likely switch to a different brand once their stock has depleted.

Brand Opportunity: To remain fresh in the minds of consumers, FMCG brands should extensively communicate and actively engage with followers on their social channels. Meanwhile, multi-category brands can also leverage this opportunity to further increase customers' order value by cross-selling other products in their portfolio.

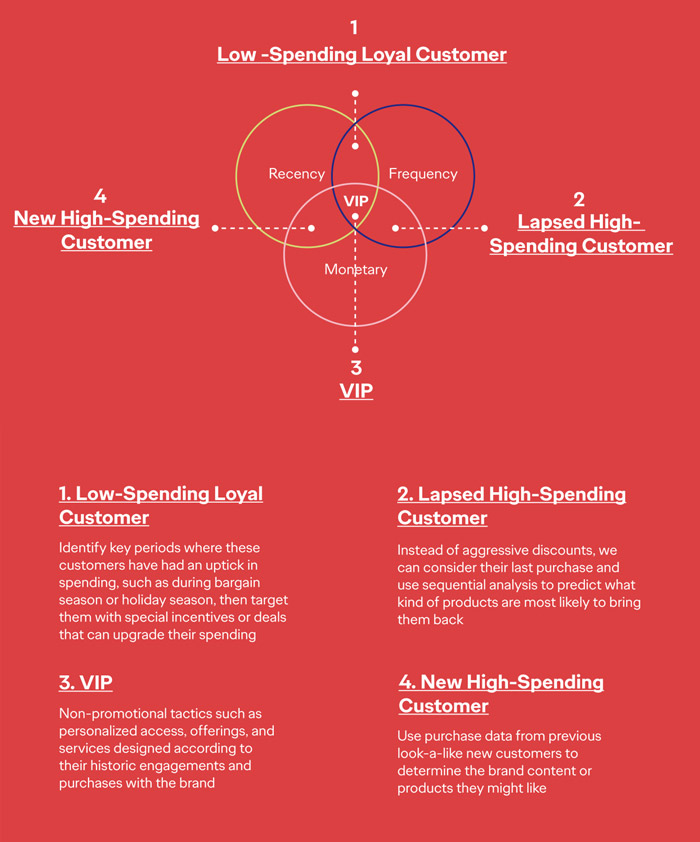

Besides identifying and maintaining high-value customers, brands can also focus on nurturing high-potential customers into VIPs. By using the RFM matrix, we can identify customers who score highly in at least 2 of the 3 dimensions (recency, frequency, monetary) and segment them into 4 key groups (Chart 4). Brands can design their communication according to insights gained from looking back at customers' previous purchase behaviors.

While the RFM model can serve as an effective systematic guideline for brands to more precisely segment and identify their top customers, it only constitutes the first step of your strategic decision-making. Understanding the impact of current events on consumer behavior and the particularities of different industries allows your communication to become more agile, helping the brand succeed in the New Normal and ultimately grow the brand's overall customer lifetime value.

Sources:

「Author」

Pires Guo

Associate Strategy Director, Social and CRM, Shanghai

「Author」

Virginia Wang

Strategist, Shanghai